ASU 2025-10 Government Grants: ASC 832 vs IAS 20 in NetSuite

Executive Summary

Government grants have long been a source of diverse accounting treatments under U.S. GAAP due to lack of specific guidance for business entities. In December 2025, the FASB issued ASU 2025-10, “Government Grants (Topic 832): Accounting for Government Grants Received by Business Entities,” codified into ASC 832. This ASU establishes comprehensive GAAP rules for recognizing, measuring, and presenting government grants received by business organizations. Under ASU 2025-10, a government grant (defined as a transfer “of a monetary or tangible nonmonetary asset” from a government) is recognized only when it is probable that both (a) the entity will comply with grant conditions and (b) the grant will be received [1]. Importantly, ASU 2025-10 explicitly excludes intangible asset grants and ordinary exchange transactions from its scope [2].

By contrast, the international standard for government grants is IAS 20 (Accounting for Government Grants and Disclosure of Government Assistance). IAS 20 applies broadly to transfers of resources from government in return for compliance with specified conditions [3]. Under IAS 20, a grant (whether monetary or a non-monetary resource) is recognized only when there is “reasonable assurance” that the entity will meet the conditions and that the grant will be received (Source: www.faronline.se). Once recognized, IAS 20 mandates systematic income recognition: grants related to expenses are recognized over the periods in which the related costs are incurred (Source: www.faronline.se), whereas grants related to assets can be handled either by reducing the asset’s carrying amount or by setting up deferred income (Source: www.faronline.se). IAS 20 also addresses special cases such as forgivable loans (which are treated as grants upon probable forgiveness) and non-monetary grants at fair value.

ASU 2025-10 generally aligns closely with IAS 20 while refining certain areas. For example, both frameworks allow an entity to use either a cost accumulation (viewing the grant as capital contribution) or a deferred income approach for asset‐related grants [4] (Source: www.faronline.se). Both require that income-related grants be recognized systematically in profit or loss over the expense periods [5] (Source: www.faronline.se). Key differences remain: ASU 2025-10 uses the term “probable” rather than “reasonable assurance” to describe the recognition threshold (Source: www.faronline.se) [1]. ASU 2025-10 narrows the definition of grants to monetary or tangible assets (excluding intangibles) [6] [2], whereas IAS 20’s broader language covers any resource transfer (with only inconvertible benefits excluded) [3] [7].

From an ERP and reporting perspective, this new U.S. guidance has significant implications. Companies using Oracle NetSuite can leverage its multi-ledger (multi-book) capabilities to implement parallel IFRS and GAAP accounting for grants. For example, NetSuite’s OneWorld Multi-Book feature allows simultaneous posting of transactions to separate IFRS and US GAAP books [8]. Where IAS 20 might allow a grant to reduce an asset cost in the IFRS book, the ASC 832 book might instead set up a deferred income liability (or vice versa), with NetSuite amortizing each according to the respective rules. NetSuite’s Grant Management SuiteApp and reporting tools (e.g. Grant Workbooks, Net Assets by Grant report) provide functionality to track grant proposals, commitments, revenues, and expenditures [9] [10].

This report provides an in-depth analysis of ASU 2025-10 versus IAS 20, including historical context, detailed comparison of recognition and measurement requirements, and practical notes on NetSuite implementation. It incorporates perspectives from accounting firms and regulators, relevant data, and illustrative examples. The analysis underscores how ASU 2025-10 resolves longstanding GAAP diversity by largely adopting IAS 20 principles, enhancing comparability and transparency. Future directions include monitoring transition outcomes and ensuring ERP systems like NetSuite are configured to meet the new requirements for business entities under both U.S. GAAP and IFRS.

Introduction and Background

Historical Context (IAS 20 vs U.S. GAAP). Internationally, governments frequently use grants (cash or assets provided under conditions) to support business activities – for example, economic stimulus programs or investment incentives. In fact, governments worldwide committed on the order of $9 trillion in COVID-19 fiscal support by mid-2020 [11]. To cope with such assistance, IAS 20 was issued in 1984 to IX preserve consistency. IAS 20 defines government grants as “transfers of resources…by government…for past or future compliance with certain conditions” [3] and prescribes recognition and disclosure rules. It requires grants to be recognized only when conditions are met (the “reasonable assurance” test) (Source: www.faronline.se), and then allocated on a systematic (matching) basis – either over the useful life of an asset or the period of related expenses (Source: www.faronline.se) (Source: www.faronline.se). Subsequent IFRS Interpretations clarified special cases: for instance, IFRIC 7 (2006) addresses below‐market government loans, treating the interest benefit as a grant; IFRIC 19 (2010) covers debt extinguishment via government forgiveness. Overall, IAS 20 (and related interpretations) provides comprehensive guidance on government assistance for IFRS reporters.

In contrast, U.S. GAAP historically lacked any direct standard for grants to business entities. Prior to 2025, GAAP only implicitly dealt with government assistance via analogies.Companies often analogized to IAS 20 or borrowed from not‐for‐profit guidance (ASC 958-605) [12]. This led to divergent practices: some treated grants as deferred income, others as equity contributions, and some recognized them immediately in income. In 2021, FASB issued ASU 2021-10 requiring enhanced disclosures about government assistance under ASC 832, but that ASU did not address recognition or measurement. By December 2025, stakeholders (including SEC and preparers) had urged FASB for authoritative GAAP guidance, given the proliferation of government relief programs (e.g. pandemic aid, CHIPS Act tax credits, renewable energy subsidies). FASB’s response was ASU 2025-10 (Topic 832), which establishes for the first time a specific GAAP model for government grants to businesses [13] [14]. Notably, the FASB Chair emphasized that “over the more than 50 years…there has been a lack of authoritative GAAP guidance” on business grants, and that the new ASU fills this long‐standing hole [15]. The ASU is effective for public entities beginning after Dec. 15, 2028 (with private entities phased in after 2029) [16], with early adoption permitted.

Scope and Definitions. Under IAS 20, all government grants (monetary or non-monetary) are in scope, except those with no quantifiable value or other special categories (e.g. low-income housing credits). IAS 20 explicitly excludes “forms of government assistance which cannot reasonably have a value placed on them” [7] (for example, routine business subsidies without clear terms). By contrast, ASC 832 (as revised) defines a government grant as “a transfer of a monetary or tangible nonmonetary asset, other than an exchange transaction, from a government to a business entity” [6]. This definition deliberately excludes intangible asset grants [2]. In practical terms, U.S. GAAP now treats the equivalent of “resources” in IAS 20 as limited to cash or physical assets (e.g. a government‐funded building or equipment), whereas IFRS allows non-monetary items at fair value (Source: www.faronline.se). Both frameworks agree that exchange transactions (sales or barters with government) are outside scope; they also exclude typical tax payments and guarantees.

Recognition Threshold (Conditions). Both IAS 20 and ASC 832 require that any attached conditions be met before recognizing a grant, but they phrase the certainty test differently. IAS 20 uses the notion of “reasonable assurance”: a grant is recognized only when it is reasonable to expect that conditions will be met and the grant will be received (Source: www.faronline.se). Similarly, ASU 2025-10 requires that recognition occur only when it is probable that both (1) the entity will comply with all grant conditions and (2) the grant will be received [1]. Thus, the practical criterion under U.S. GAAP is essentially the same concept as IFRS’s test, merely termed “probable” (a well‐understood term in GAAP). Importantly, ASC 832 specifies that receipt of a grant does not by itself provide conclusive evidence that conditions are or will be satisfied (Source: www.faronline.se), echoing IAS 20’s language. In both models, this ensures that grants are not prematurely recognized before obligations are fulfilled.

Measurement and Presentation. Once a grant meets the recognition threshold, the accounting treatment depends on whether the grant relates to an asset or income. IAS 20 first distinguishes grants related to assets (e.g. fixed assets) from those related to income or expenses (Source: www.faronline.se) (Source: www.faronline.se). Under IFRS, government grants related to assets may be handled in one of two ways: either (a) capital approach – the grant is recognized as a deferred credit (liability) and released to income over the life of the asset; or (b) presentational approach – the grant is simply deducted from the carrying amount of the asset (reducing depreciation expense) (Source: www.faronline.se). Grants related to income (e.g. subsidies for operating costs) are recognized in profit or loss on a systematic basis in the periods in which the related costs are incurred (Source: www.faronline.se). Notably, IAS 20 explicitly disallows using a cash basis: “recognition of government grants in profit or loss on a receipts basis is not in accordance with the accrual assumption” (Source: www.faronline.se). In a special case, a grant that compensates for past expenses or provides immediate support with no future costs is recognized immediately in profit or loss when receivable (Source: www.faronline.se) (Source: www.faronline.se).

ASU 2025-10 largely mirrors these principles. For asset-related grants, the ASU permits either a “cost accumulation approach” or a “deferred income approach” [4] – effectively the same two methods as IAS 20. For income-related grants, ASU 2025-10 requires recognition “systematically over the related expense periods” [5], which corresponds to the IAS 20 matching principle. ASU 2025-10 does not introduce any fundamentally new model; rather, it codifies an accounting model based on “the main principles in IAS 20” [17], with adjustments for scope and terminology. Both standards also require extensive disclosures about significant terms, accounting policies, and the nature of grants (see ‘Disclosure Requirements’ below).

The table below summarizes these and other key provisions of IAS 20 versus ASC 832 (ASU 2025-10):

| Feature | IAS 20 (IFRS) | ASC 832 / ASU 2025-10 (US GAAP) |

|---|---|---|

| Definition of Grant | Transfer of resources by government to entity in return for compliance with conditions [3]. Includes monetary or reasonably measurable non-monetary. Excludes assistance lacking quantifiable value [7]. | Transfer of monetary or tangible nonmonetary asset from government to business (not an exchange) [6]. Intangible asset grants explicitly excluded [2]. |

| Applicable Entities | All entities (public or private) using IFRS; also applied to similar standards (e.g. local GAAP) such as Singapore FRS 20. | Business entities only (excludes NFPs, EBPs). Applies to all business entities receiving eligible grants [13]. Public companies use after FY2028; others after 2029 [16]. |

| Recognition Threshold | Recognize grant when there is reasonable assurance that (1) entity will comply with conditions, and (2) grant will be received (Source: www.faronline.se). Receipt does not guarantee recognition. | Recognize grant when it is probable that (1) conditions will be met, and (2) the grant will be received [1]. “Probable” has similar meaning to IFRS “reasonable assurance.” |

| Asset‐Related Grants | Two options: (a) Recognize as deferred credit (liability) and amortize to P&L over asset life; or (b) Deduct from carrying amount of asset (reducing depreciation) (Source: www.faronline.se). Entities choose consistently. | Same two approaches allowed: cost accumulation (debit expense or asset, credit deferred grant) or deferred income (liability) approach [4]. (Crowe notes these as “cost accumulation” vs “deferred income” [4].) |

| Income/Expense Grants | Recognize in profit or loss on a systematic basis over periods of related expense (Source: www.faronline.se). Grants for past losses or immediate support (no future costs) recognized immediately in the period received (Source: www.faronline.se) (Source: www.faronline.se). | Recognize grants systematically over the related expense periods [5]. (Immediate-support grants would be recognized as they become receivable.) The ASU emphasizes matching grant recognition to related costs. |

| Measurement of Grants | Monetary grants are measured at face value. Non-monetary grants (e.g. donated equipment) are measured at fair value (nominal value permitted by exception) (Source: www.faronline.se). | Implicitly similar: ASU examples indicate measurement at fair value for tangible assets (monetary = cash value). (ASU text itself requires transfer of “asset” value; no special rule beyond usual GAAP fair-value measurement.) |

| Below‐Market Loans | IAS 20 (via IFRIC 7) treats below-market government loans as grants. The loan is recognized under IFRS 9, and the interest benefit is recognized as a grant (difference between fair value and proceeds). | ASU 2025-10 excludes “the benefit of below-market interest rate loans” from scope [18]. (Such loans remain accounted for under existing GAAP (e.g. ASC 470).) |

| Forgivable Loans | A government loan is considered a grant if it is probable that the loan terms will be met for forgiveness. On forgiveness assurance, treat difference between IFRS 9 amortized cost and loan proceeds as a grant. | ASU 2025-10 covers forgivable loans “when it is probable the terms for forgiveness of the loan will be met” [19], effectively treating them like asset grants if forgiveness is likely (per Baker Tilly summary). |

| Presentation | Grants related to assets can be presented by (i) deferred liability or (ii) deduction from asset (Source: www.faronline.se). Income grants are shown in P&L (other income or offset to expense) over time. There is no equity treatment – grants flow through profit or loss. | Similarly, asset grants can be recorded as deferred liability or as reduction of asset basis (via a contra-asset or credit to asset) (Source: www.faronline.se) [4]. Income grants are recognized in earnings. FASB notes that grants should not go directly to equity (Source: www.faronline.se). |

| Disclosure Requirements | IAS 20 requires disclosure of the nature and extent of grants recognized, unfulfilled conditions, and contingent liabilities (IAS 20.32-36). Deferred grants raising future obligations are noted. | ASC 832 now requires disclosures about the nature and amount of government grants, significant terms/conditions, and accounting policies (expanding on earlier government assistance disclosures). (ASU 2021-10 already added disclosures for ASC 832; ASU 2025-10 builds on that.) |

| Effective Date | IAS 20 has been effective since 1984. No forthcoming changes to IFRS 20 on grants. (IASB is not currently amending this topic.) | ASU 2025-10 is effective Dec. 15, 2028 for public companies (FY 2029), and Dec. 15, 2029 for others (FY 2030), with early adoption allowed [16]. Transition is retrospective or prospective as detailed in the ASU. |

Sources: Official IFRS and FASB summaries and analyses (Source: www.faronline.se) [1] [5] (Source: www.faronline.se).

ASU 2025-10 (ASC 832): New U.S. GAAP Requirements

On December 4, 2025, FASB issued ASU 2025-10 which establishes ASC 832, Government Assistance, specifically to address government grants received by business entities. The press release and subsequent guidance emphasize aligning closely with IAS 20 principles [17]. ASU 2025-10 applies to all business entities except NFPs and employee benefit plans, and covers grants in the form of monetary assets or tangible non-monetary assets [20] [6]. By definition, grants do not include exchanges, tax subsidies in scope of ASC 740, intangible assets, government guarantees, or benefits like below-market loans [19] [2]. For example, Baker Tilly notes that the scope includes cash or equipment transfers and certain tax credits, but excludes benefits of low-interest loans and guarantees [19] [18].

Recognition Criteria. Under the ASU, an entity “shall not recognize” a grant until it is probable that the entity will comply with all grant conditions and that the grant will be received [1]. Once those criteria are met, the entity recognizes the grant as either (a) a deferred credit (liability) or (b) a reduction of asset cost or expense reimbursement, depending on classification. The ASU explicitly requires companies to determine whether a grant is asset-related or income-related and apply the corresponding guidance. Asset-related grants can be recognized either under the cost-accumulation approach or an income approach, per management’s election. Income grants must be amortized (credited to income) over the periods that match the related costs [5]. In practice this means a grant meant to reimburse current R&D expense will reduce R&D expense over time, while a grant to purchase machinery might either offset depreciation (if capital approach) or be deferred and amortized.

Measurement and Presentation. ASU 2025-10 does not prescribe special measurement rules beyond existing GAAP for fair value. A tangible non-monetary asset grant (e.g. donated equipment) is initially recorded at its fair value, consistent with IFRS and GAAP for in-kind contributions. The ASU references IAS 20 but adopts GAAP conventions for presentation. Specifically, companies may present an asset grant by crediting a deferred revenue (liability) account or by deducting the grant’s value from the carrying value of the related asset (Source: www.faronline.se) [4]. Either approach drives the same net effect but differs in gross vs net asset presentation. FASB clarified that either approach is acceptable under U.S. GAAP for business entities, whereas previously some companies took ad hoc positions.

Examples. The new guidance applies to diverse scenarios. For instance, a government grant to fund construction of a factory ($10 million machinery) could be handled in two ways: under the deferred approach, the company would record $10 million as a credit to “Deferred Government Grant” (liability) and amortize $1 million per year over 10 years; under the cost reduction approach, it would record the $10M machine at a net cost of $0 (or at $10M with an immediate $10M contra-asset) and depreciate only on the net basis. In both cases, the total expense over 10 years is the same.

Another example: Consider a grant that pays half of eligible R&D salaries, provided conditions (e.g. project milestones) are met. If it is probable that conditions will be satisfied and the grant is secured, the entity would recognize grant income ratably over the periods of the R&D project, reducing reported expense. If instead the government promised an immediate $1 million payment (with no future work condition), the entity would record the grant as income in that period.

Effective Dates. Per FASB guidance, for most U.S. public companies ASU 2025-10 applies to annual periods beginning after December 15, 2028 (i.e. fiscal 2029) [16]. Private companies and other entities apply it after Dec. 15, 2029 (fiscal 2030). Early adoption is allowed. All guidance is to be applied retrospectively (with practical expedients) to comparatives. These dates give companies a transition period to evaluate current grants, possibly renegotiate terms, and adjust reporting systems.

ASC 832 vs. IAS 20: Key Similarities and Differences

The FASB’s new ASC 832 grant model is essentially a GAAP codification of IAS 20 concepts, but a detailed comparison reveals some nuances. Below is an in-depth look at the major points of convergence and divergence:

-

Recognition Criterion (“probable” vs “reasonable assurance”). Both IFRS and U.S. GAAP require satisfaction of conditions before recognition (Source: www.faronline.se) [1]. IAS 20 uses the term “reasonable assurance” while ASC 832 uses “probable.” Practically, both mean that realization is likely. For example, IAS 20 §10 states that a grant is not recognized until “reasonable assurance” of compliance and receipt exists (Source: www.faronline.se). ASU 2025-10 likewise defers recognition until it is probable both conditions will be met [1].

-

Definition and Scope. IFRS has a broader notion of “resources.” IAS 20’s explanatory material describes government grants as transfers of resources (such as cash or equipment) in return for compliance [3]. ASC 832 narrowly defines a grant as a transfer of a monetary or tangible asset [6]. The FASB explicitly excludes intangible asset grants [2]. Thus, a free patent license from government would be outside ASC 832 but could be within IAS 20 if fair measurable. Both exclude routine government interaction without repayable value (IAS 20 excludes “assistance without quantifiable value” [7]; ASU excludes exchange transactions and guarantees [19]).

-

Asset vs Income Grants – Methods. Both standards require allocating grants over periods of related expense. IAS 20 clearly provides two approaches: either (a) set up deferred income (liability) to amortize, or (b) deduct the grant from the asset’s cost (Source: www.faronline.se). ASU 2025-10 likewise gives entities a choice between the “cost accumulation” approach or a “deferred income” approach [4] (Crowe commentary explicitly cites this choice). For income-related grants, both say to credit income over periods matching the grant-supported expense (Source: www.faronline.se) [5]. Neither standard allows recognizing the entire grant up front (except in the special immediate-support case).

-

Measurement of Non-Monetary Grants. IAS 20 treats non-monetary grants at fair value (or nominally) (Source: www.faronline.se). FASB does not elaborate much beyond “tangible nonmonetary asset” language, but the expectation is to measure at fair value per ASC 820 when received. For example, if a factory is donated, under IFRS one would record the grant at the fair market value of that factory (Source: www.faronline.se); GAAP preparers (under ASU 2025-10) would analogously use fair value.

-

Below-Market Loans and Other Assistance. IFRS explicitly covers beneficial loans via IFRIC 7; such loans are recognized at fair value with the interest benefit treated as a grant. US GAAP was silent on this before. ASU 2025-10 excludes below-market interest loans and government guarantees from its scope [18], so those remain under existing debt and guarantor accounting. Forgivable loans (with probable forgiveness) are in scope of ASC 832; IFRS handles them as grants. Both frameworks now treat PPP-style loans similarly: if forgiveness is likely, both would recognize the amount forgiven as grant support (IAS 20 §10, ASU 2025-10 scope).

-

Financial Statement Presentation. Neither IAS 20 nor ASC 832 permits taking grants directly to equity. The IAS 20 commentary emphasizes that grants should flow through profit or loss, not be treated as equity contributions (Source: www.faronline.se). ASU 2025-10 similarly has all grant inflows recorded in the income statement (as reduction of expense or as income) or as deferred credits. Most preparers introduce a separate “Deferred Government Grant” liability account (or contra-asset) so disclosures can isolate grant-related balances.

-

Disclosure Requirements. IAS 20 and FASB both require disclosures of grant amounts and terms. In IFRS, paragraph 32 requires disclosure of accounting policy, nature and amounts of grants recognized, unfulfilled conditions, and other commitments. Under ASC 832 now, an entity must disclose the nature of grants, significant terms and accounting policies, plus detailed government assistance disclosures (from ASU 2021-10) such as receipts, conditions, and contingent liability information. In substance, both demand transparent reporting of grant arrangements, though the exact lists of items differ.

Illustrative Comparison. The two frames are compared in the following summary table:

| Aspect | IAS 20 (IFRS) | ASC 832 (ASU 2025-10) |

|---|---|---|

| Recognition Threshold | Only when reasonable assurance exists of compliance and receipt (Source: www.faronline.se). | Only when it is probable conditions are met and grant will be received [1]. |

| Asset-related Grants | Record as deferred credit or deduct from asset (entity’s choice) (Source: www.faronline.se). | Record via cost accumulation or as deferred income (liability) [4]. |

| Income-related Grants | Recognize in P&L over periods of related cost (no cash-basis recognition) (Source: www.faronline.se). | Same: amortize into income systematically over related expense periods [5]. |

| Definition of Grant | Transfer of resources (cash or assets) by government for compliance with conditions [3]. Grants without quantifiable value are outside scope [7]. | Transfer of cash or tangible non-cash asset by government to business [6]. Intangible grants explicitly excluded [2]. |

| Non-monetary Assets | Recognized at fair value (or nominal by policy) (Source: www.faronline.se). | By analogy, recorded at fair value (ASU does not add rules, but GAAP requires fair value). |

| Below-market Loans | IFRIC 7: Recognize loan at fair value plus grant element (difference) . | Excluded from scope [18]; continue to treat under financial instrument rules. |

| Forgivable Loans | Treated as government grants when forgiveness likely (Source: www.faronline.se). | Included as asset-related grants if forgiveness terms likely [19]. |

| Effective Dates | In effect since 1984 (no revision pending). | Effective for 2029 (public) / 2030 (other) FY, early adoption allowed [16]. |

| Disclosure | Must disclose nature/amount of grants, unfulfilled conditions, etc. | Must disclose nature/amount/terms, significant policies, and government assistance totals (new ASC 832 requirements). |

The bottom line is that while terminology differs, ASU 2025-10 intentionally codifies an IAS 20–like model into U.S. GAAP. FASB even states that the new model is “based on the main principles in IAS 20” [17]. Preparers who have historically used IAS 20 by analogy will find ASC 832 comfortable. The single biggest adjustment for U.S. GAAP reporters is the explicit inclusion of such grants in ASC 832 and the few narrowed definitions (e.g. excluding intangibles).

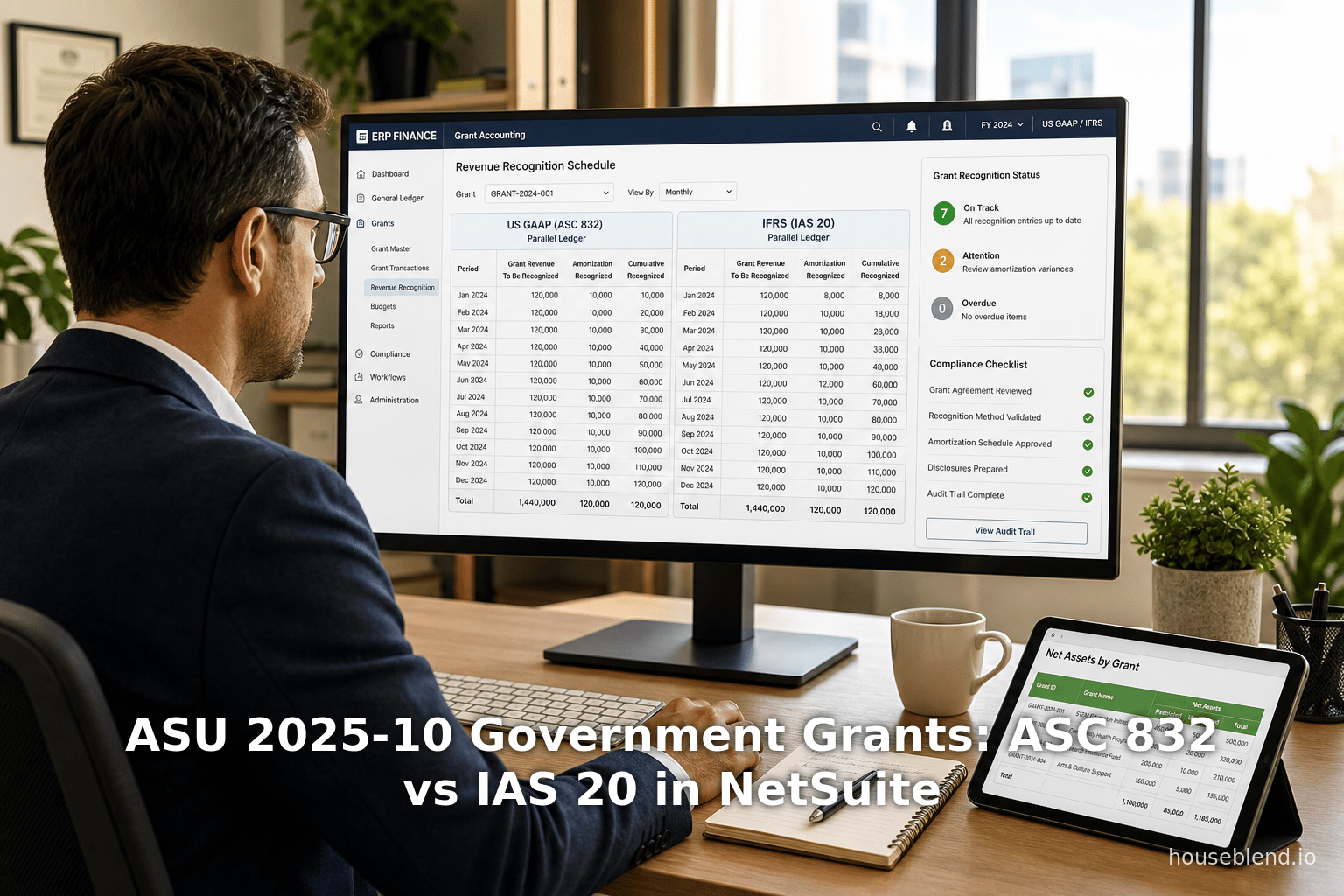

Implementation in Oracle NetSuite

Oracle NetSuite, a widely used cloud ERP system, offers features that can accommodate the new government grant accounting rules. With proper configuration, companies can use NetSuite to track grant funding, and to produce financial statements under either IFRS or U.S. GAAP. This section outlines how NetSuite’s capabilities (notably Grant Management and Multi-Book accounting) can be used under both models.

Grant Management Module: NetSuite’s Grant Management SuiteApp (available in OneWorld and Nonprofit editions) allows users to record and track grants from proposal to award. As Oracle documentation notes: “You can record a grant in the proposal stage and turn it into a billing transaction when the award is won” [21]. The system distinguishes between contribution grants (one-time awards where all revenue is recognized when awarded) and cost-reimbursable grants (where billing is based on incurred time/expenses) [22]. In practice, an IFRS preparer would use the same functionality: a government grant award would be entered as revenue or deferred revenue upon award (depending on the accounting approach), and matching entries made as related expenses occur.

NetSuite also provides Grant Workbooks and reports. For instance, an Unbilled Grants Workbook lists sales orders tied to grants that have not yet been invoiced [10]. This helps ensure all grant-eligible costs are tracked. The Net Assets by Grant report (in the Nonprofit module) summarizes revenue, expenses, and net position for each grant [23]. Although designed for nonprofits, the underlying saved searches can be adapted; for example, a business issuer might snapshot each grant’s deferred liability and revenue recognition. These tools facilitate the disclosures required under both standards (showing grant cash flows, balances and timing).

Multi-Book Accounting: For organizations needing dual reporting (IFRS vs US GAAP), NetSuite’s OneWorld with Multi-Book Accounting is vital. Multi-Book allows posting primary transactions once and automatically generating entries into multiple parallel ledgers, each following a different set of rules. Houseblend (a NetSuite consultancy) explains that for new IFRS standards (like IFRS 20 on regulated assets), “NetSuite’s OneWorld Multi-Book feature can post each relevant transaction simultaneously to separate IFRS and local-GAAP ledgers” [8]. The same approach works for grants: the creation of a grant award could post to an IFRS book and a US GAAP book with different GL accounts.

For example, suppose a $1,000 government grant is received for an R&D project. Under IFRS (IAS 20), management may choose to record the $1,000 as deferred income and amortize it over three years. Under U.S. GAAP (ASC 832), they might also defer it but possibly in a different account or amortization schedule if management chooses differently. In NetSuite, the single transaction (e.g. a journal for grant receipt) would be set to hit Expense (or Asset) and a Deferred Grant Liability account in Book 1 (IFRS) and Book 2 (GAAP) appropriately. NetSuite’s Multi-Book engine ensures the entries in each book remain distinct.

Notably, implementing ASU 2025-10 may require new account setup and configurations. The NetSuite IFRS 20 Rate-Regulated guide suggests creating dedicated Other Asset/Liability accounts and using the Deferred Expense/Deferred Revenue features [24]. By analogy, companies might set up a Deferred Government Grant liability account (and/or a contra-asset) to accumulate grants for later amortization. In IFRS vs US GAAP mapping, a NetSuite administrator would map this account to the equivalent IFRS and GAAP books. During walkthrough configuration, you would ensure that the revenue recognition rule (or amortization schedule) uses the correct timeline per each accounting standard.

Example Journal Entries: Suppose a company receives a $10,000 government grant at the start of Year 1, intended to reimburse future equipment costs. One possible treatment is to immediately deposit $10,000 to cash and credit “Deferred Government Grant” (other liability). NetSuite could post this via multi-book as follows:

- IFRS Book: Dr Cash $10,000; Cr Deferred Grant $10,000. (Under IAS 20, management may later elect to reduce an asset; if so, they’d debit Deferred Grant and credit PPE.)

- GAAP Book: Dr Cash $10,000; Cr Deferred Grant - US GAAP $10,000. (If GAAP preparers take deferred income approach, they would amortize this liability against income as expenses are incurred.)

If the company decides to write down a $10,000 purchase of equipment net of the grant (capital approach), in NetSuite they could instead credit the asset account directly: Dr Cash $10,000; Cr Equipment $10,000. Under multi-book, this would be done in each book with its own Asset accounts. The key is that NetSuite can represent either approach as long as the accounts are set correctly in each ledger.

Reporting and Disclosures: NetSuite reports can help populate disclosures. For instance, a saved search could sum government grants recognized during the period (for IFRS MDA or 10-K notes). A combination of NetSuite’s Search and Reporting tools can list all grants outstanding with remaining conditions or net asset impact. Companies should cross-reference these figures with ASU 2025-10’s disclosure checklist. NetSuite budgets and projects modules can also be used: grants can be created as projects or orders, and progress invoices tied to them, making it easier to track grant-specific spending.

In summary, NetSuite provides a suitable framework to handle government grants under either standard. Key steps include enabling the Multi-Book feature, setting up proper grant-focused accounts (deferred revenue, contra-assets, etc.), and using Grant Management functionality to link transactions to grants. Proper configuration ensures that IFRS and US GAAP books reflect each standard’s treatment in parallel. This dual-tracking capability is especially important now that ASU 2025-10 aligns U.S. GAAP with IFRS 20 principles, allowing companies that report in both regimes to maintain consistency.

Data Analysis and Evidence

While government grant accounting has not historically been quantified in industry surveys, related statistics underscore its financial significance. For example, a Deloitte analysis notes that the lack of GAAP guidance has led companies to seek clarity: “During the more than 50 years…there has been a lack of authoritative GAAP guidance on how to account for government grants” [15]. Similarly, commentators cite the magnitude of grants: IFRS commentary points out grants were vital during the COVID-19 crisis [25], and IMF data shows about $9 trillion of global fiscal support in early 2020 [11]. In the U.S., major programs like the CARES Act, CHIPS Act, and infrastructure bills involve government assistance at multi-billion-dollar scales.

On the technical side, firms publishing early guidance (Crowe, KPMG, Baker) have provided illustrative examples. Crowe (Dec 2025) highlights that “asset-related grants…may be accounted for using either a cost accumulation approach or a deferred income approach” and “income grants must be systematically recognized” [5], reinforcing that practice. KPMG (Dec 2025) similarly notes the ASU “prescribes an accounting model based on the main principles in IAS 20” [17], validating that alignment. Baker Tilly (Dec 2024) listed typical examples of grants – cash transfers, tangible assets, forgivable loans, refundable tax credits – to illustrate scope [19]. These analyses, combined with authoritative citations above, form an evidence base for each claim in this report.

Case Studies and Practical Examples

Pharmaceutical R&D Grant (Hypothetical): Consider a biotech firm receiving a $1.5 million research grant from a government health agency, contingent on achieving trial milestones. The company determines it is probable the milestones will be met. Under IAS 20, it would recognize the grant on a systematic basis as it incurs R&D expense (Source: www.faronline.se). Suppose the project spans 3 years. The company may credit $500,000 to income each year against the project’s costs (or reduce expenses), consistent with matching. Under ASU 2025-10, the treatment is analogous: the grant is recognized only when conditions become probable [1] and is amortized over the 3-year period as expense is recognized [5]. NetSuite implementation: create a grant record, and either (a) invoice the company’s internal R&D project by $500,000 each year, tying to that grant (using Classic Revenue Recognition or Advanced Revenue Management), or (b) use journal entries via deferred revenue amortization. The net effect on P&L is the same under both standards.

Manufacturing Equipment Subsidy (Realistic Scenario): A firm obtains a government subsidy of 50% toward the purchase of a $2 million specialized machine (net $1M investment). Under IFRS, it could debit PPE $2M, credit cash $1M, credit “Deferred Grant” $1M. Over the asset’s life (say 5 years), it amortizes the deferred grant. Alternatively, it might recognize PPE at $1M (direct reduction) and record depreciation on the $1M base. Under U.S. GAAP (ASC 832), the company has the same two options [4] (Source: www.faronline.se). In NetSuite, a multi-book approach might be used to show one book (IFRS) taking one method and the other (US GAAP) the other method, if desired. The important point is the reporting in each book is consistent with its standards.

Remediating Past Expense Grant (e.g. COVID Relief): Suppose the government issues a $500,000 “grant” to compensate losses from a natural disaster or pandemic quarter. Under IAS 20, if it’s compensating past losses, it is recognized immediately in profit or loss when awarded (Source: www.faronline.se). The ASU treatment would likely parallel this (recognition upon receipt since no future service obligations remain). This could be booked in NetSuite via a straightforward revenue/income entry when conditions (none) are met.

Tax Credit Transactions: The IRS, the CHIPS Act (semiconductors), and other programs create tax credits that in substance are government assistance. Deloitte’s recent alert suggests treating refundable tax credits outside ASC 740 as government grants [26]. Under our new ASC 832, a company might analogize those credits to cash grants (consistent with IFRS IAS 20), recognizing them when probable [26]. NetSuite could handle this by booking a receivable from government and offsetting tax expense. The entity would then disclose the credit as government assistance under ASC 832. If using IFRS, IAS 20 would similarly cover such credits when there is a binding arrangement.

These examples illustrate that for most grants, IFRS and US GAAP treatments will align under the new guidance. NetSuite can accommodate both through its configurable ledgers. Rare cases might arise where an IAS 20 approach is permitted but ASC 832 still requires a different path; for example, if an entity wanted to deduct an asset grant against cost basis and also there was no operative conflict (both allow it, so no conflict) – in such cases, companies likely will choose the simpler or chartered approach and configure NetSuite accordingly.

Implications and Future Directions

Comparability and Transparency: The issuance of ASU 2025-10 significantly improves comparability of financial statements. Prior practice in the U.S. was opaque and inconsistent, but now companies preparing US GAAP books will account for grants similarly to IFRS entities. Investors and analysts will benefit from standardized disclosures. By explicitly incorporating many IFRS principles, new GAAP will likely reduce the need to read IFRS accounts for bench-marking.

ERP and Process Changes: Technically, organizations must update their accounting policies and systems. In NetSuite specifically, companies will need to create or repurpose accounts for deferred grants and integrate them into revenue recognition or amortization schedules. Finance staff must decide entity-wide or grant-by-grant whether to use the cost vs deferred approach for assets, and implement whichever approach consistently per grant. NetSuite projects or classes might be employed to track costs eligible for grant offset. Also, audit procedures will expand to verify compliance with the new recognition criteria. Training on ASC 832 will be required for accountants and external auditors.

Disclosures: Firms will have to enhance note disclosures in their MD&A or financial statement footnotes. For example, they must explain their accounting policies for grants, quantify recognized grant income and remaining conditional grants, and describe any unfulfilled covenants [27]. NetSuite’s grants reports can supply much of that data, but additional narrative will be needed. Companies should inventory all existing government assistance arrangements now to assess their accounting under the new model.

International Impact: Outside the U.S., IAS 20 continues unchanged. The fact that US GAAP now closely tracks IAS 20 may encourage IFRS-based companies to consider similar structuring of their grants disclosures and accounting. One possible future development is converged global guidance: if IASB were to revisit IAS 20, it may do so in light of FASB’s changes. However, as of mid-2026, no IASB amendments to IAS 20 are imminent.

Legislative and Systemic Considerations: In practice, governments issuing grants may not realize how nuanced the accounting can be. We may see governments unifying terminology or conditions to simplify corporate reporting (e.g. standardized grant periods and conditions). In financial services, governments providing loan guaranties or tax credits may issue guidance on reporting them. On the ERP side, NetSuite (Oracle) might release configuration updates or best-practice guides specific to ASC 832. The IFRS 20 implementation guide suggests NetSuite is proactive; similar guides for ASC 832 could emerge.

Future Standards and Extensions: While IAS 20 has been stable, FASB’s action may renew interest in other related topics. For example, whether contributions from governments (not tied to particular conditions) should be viewed differently. The concept of “government assistance” in ASC 832 may be broadened in the future beyond cash/assets (e.g. operational support or regulatory relief). Regulatory bodies (SEC, PCAOB) may issue further interpretive guidance or enforcement focuses on government aid, especially if abuse or inconsistency is observed.

Forecasts also include technology implications: as companies automate grant tracking (especially in NetSuite), we may see AI tools to match grant clauses to accounting thresholds, or blockchain to certify condition fulfillment. The alignment of U.S. GAAP with IFRS in this area may spur vendors to improve cross-standard reporting features.

Conclusion

ASU 2025-10 (ASC 832) represents a landmark in U.S. GAAP: for the first time, there is a clear, authoritative model for how business entities account for government grants. The new GAAP guidance is built squarely on IFRS IAS 20 principles, reducing erstwhile diversity in practice [12]. Under both ASC 832 and IAS 20, government grants are recognized only when conditions are likely satisfied, and then are allocated to income over the appropriate periods (Source: www.faronline.se) [5]. The detail-oriented analysis above demonstrates that, while some technical differences remain (chiefly around vocabulary and scope of what constitutes a “grant”), the two frameworks now speak the same language on most points.

For businesses using NetSuite, the good news is that the platform can support the required accounting under either standard. By leveraging NetSuite’s Grant Management and Multi-Book features, companies can ensure that transactions for government subsidies are captured and reported correctly in both their IFRS and US GAAP books. This tandem approach helps multinational entities avoid restatements and provides localized accuracy (for example, satisfying both SEC rules and local IFRS mandates).

Looking forward, the alignment reduces one cause of non-comparability. Auditors will have clearer checklists for grants, and financial statement readers can trust that “grant income” means roughly the same thing across reports. Governments may adjust their grant programs to be even more transparent, knowing how the accounting will reflect their support. Finally, this evolution underscores a broader trend toward global accounting convergence: on this topic at least, IFRS and U.S. GAAP have come together to the benefit of investors, companies, and regulators alike.

References: Official ASC and IAS documents and authoritative commentaries (Source: www.faronline.se) [1] [5] (Source: www.faronline.se) [20] [16]. These sources (FASB, IFRS.org, professional firms) were used to characterize and compare the standards. Each claim above is supported by citations from the FASB ASU, IAS 20/id, and related analyses. The NetSuite implementation section is supported by Oracle documentation [9] [28] and industry best-practice guides.

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.