Hedge Accounting Guide: IFRS 9 vs ASC 815 Comparison

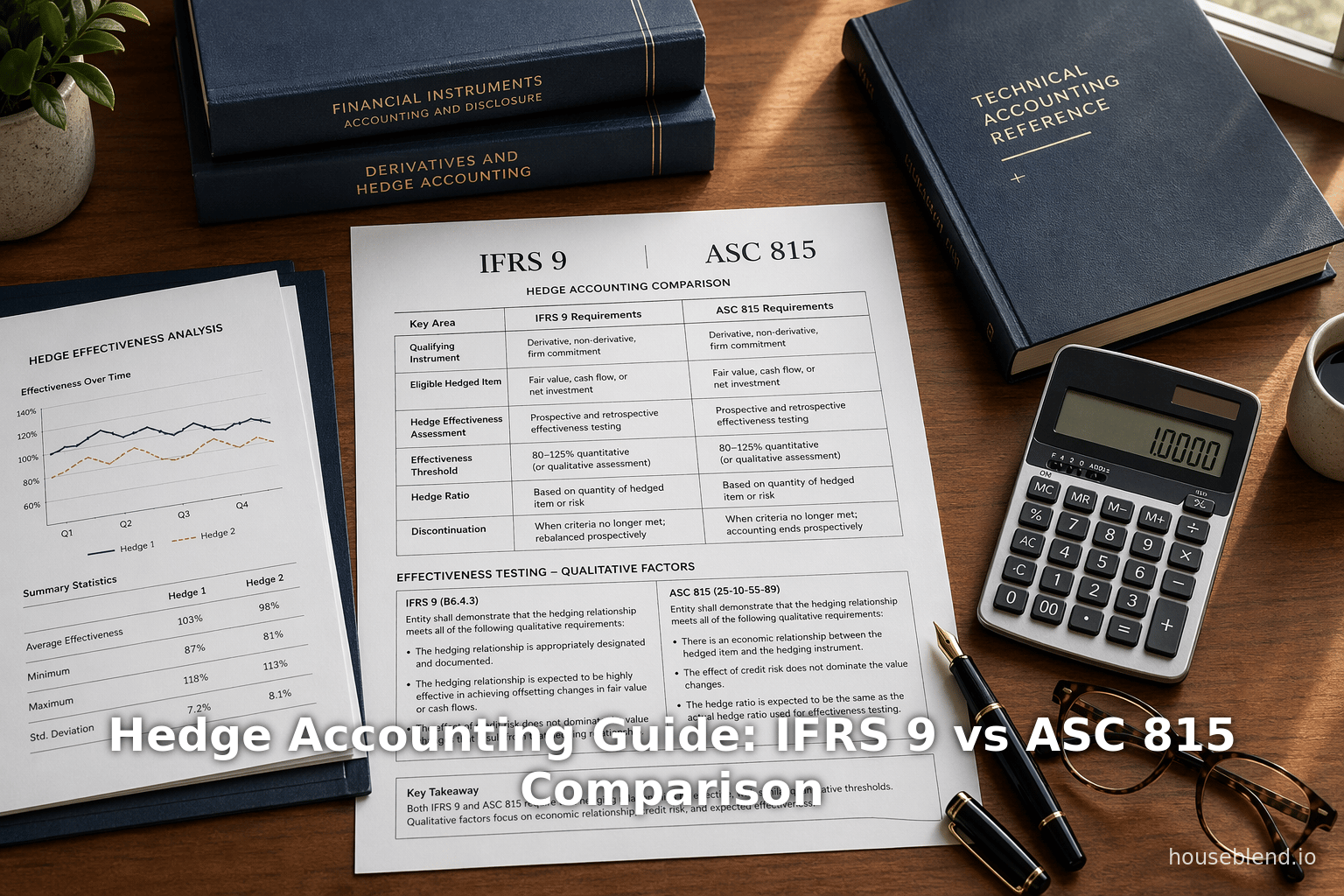

Executive Summary

Hedge accounting is a specialized method of financial reporting used by corporate treasuries to align the accounting outcomes of derivatives with their underlying risk management activities. Under IFRS 9 (the International Financial Reporting Standard for financial instruments) and US GAAP ASC 815 (Accounting Standards Codification Topic 815), hedge accounting rules allow companies to reduce artificial profit-and-loss (P&L) volatility that arises from marking hedging instruments to market, by matching the timing of gains/losses on hedges with those of the hedged items. While both IFRS 9 and ASC 815 provide frameworks for hedge accounting, they differ significantly in their approach. Key differences include: effectiveness testing (IFRS 9 uses a principles-based “economic relationship” test vs. ASC 815’s bright-line 80–125% rule) [1]; measurement of ineffectiveness (IFRS 9 measures only excess ineffectiveness beyond a “lower-of” test [2], whereas under US GAAP all fair value changes are taken to OCI for cash flow hedges [3]); dedesignation rules (IFRS 9 forbids voluntary dedesignation so long as risk objectives remain unchanged [4], while US GAAP permits it); and hedged item flexibility (IFRS 9 allows hedging of aggregated or risk components that are “separately identifiable and reliably measurable” [5], whereas ASC 815 is more restrictive). Table 1 below summarizes the principal IFRS 9 vs. ASC 815 hedge accounting differences discussed in the literature and accounting guides.

| Feature | IFRS 9 (IFRS) | ASC 815 (US GAAP) |

|---|---|---|

| Effectiveness Test | Principles-based test of “economic relationship” – qualitative methods allowed; no 80–125% band [1]; IFRS 9 also requires credit risk not to dominate and the hedge ratio to match the hedged quantities [1]. “Rebalancing” allowed (adjust hedge ratio without dedesignation) [6]. | Bright-line 80–125% effectiveness range; forward-looking test with dual – prospective and retrospective – assessments required each period [1] [7]; no rebalancing concept (changes in terms may force a dedesignation [6]). |

| Ineffectiveness Measurement | Only the amount by which the cumulative change in fair value of the hedging instrument exceeds the hedged item is recognized in P&L. The rest (effective portion) passes through OCI and is reclassified when the hedged item affects earnings [2] [8]. Time-value-of-money must be considered in valuing hedged item (present value basis) [9]. | No separate ineffectiveness measure: essentially all fair value changes of the hedging instrument (effective portion) are taken to OCI for cash flow hedges [3]; ineffective portion (if any) hits P/L. Net investment hedges use CTA section of OCI. |

| Testing Frequency | Requires a prospective effectiveness assessment at inception and at least when interim/annual statements are prepared (“ongoing basis”) [7]. No mandatory retrospective test is required. | Requires both prospective and retrospective effectiveness testing at inception and at least quarterly when financials are issued [7]. |

| Dedesignation | Voluntary dedesignation is not permitted if the hedging relationship still meets risk-management objectives [4]. Dedesignation is only required if the original objectives change or criteria are no longer met. | Voluntary dedesignation is permitted at any time after inception, without changing terms [4]. |

| Risk Components | More flexible. For non-financial items, entities may hedge risk components that are not contractually specified, provided they are separately identifiable and reliably measurable (e.g. benchmark interest rate component) [5]. | More restrictive. Risk components of non-financial hedges must generally be contractually specified. For example, only entirely specified interest rate portions may be hedged [5]. |

| Foreign Currency & Business Combos | Allows hedging of foreign currency exposures in a business combination (e.g. forecasted foreign-currency cash flows of an acquiree) under FV or CF models [10]. Also permits net investment hedges of a subsidiary through the direct consolidation method even when intermediate subsidiaries have different functional currencies [11]. | Does not allow hedging anticipated business combination cash flows or firm commitments related to combinations [10]. Does not permit net investment hedging of a lower-tier subsidiary if an intermediate entity has a different functional currency [11]. |

| Shortcut Method | No specific shortcut method. All hedges require the usual documentation/testing rules. IFRS 9’s principle-based approach means entities can combine options, forwards, etc., but must test them for effectiveness (although reassessment may be qualitative) [1]. | Allows a “shortcut” method for certain interest rate swaps: if critical terms match exactly, one may assume perfect effectiveness without quantitative testing. No analogous shortcut in IFRS 9 [12]. |

| Aggregated Items (Macro Hedge) | Permits hedging of aggregated exposures (e.g. </current_article_content>combination of a debt plus derivative) as one hedged item [13]. Also explicitly acknowledges macro (portfolio) hedging in IFRS 9. | Does not allow an aggregated exposure (compound of a non-derivative and a derivative) to be the hedged item because the components lack the same risk [13] [14]. US GAAP does allow portfolio layering (PLM) for debt (FASB ASU 2022-01) [15], but macro hedging is generally more limited. |

| Hedge Ratio Adjustments | “Rebalancing” allowed: an entity can adjust (re-balance) the hedged ratios if economic equivalence still holds, without dedesignating [6]. | No rebalancing concept; modifying hedge terms often requires dedesignation and redesignation of the hedge [6]. |

| IBOR (Reference Rate Reform) Relief | IFRS 9 provides a practical expedient to allow updating the effective interest rate for the new benchmark when reform triggers a contract modification, without breaking hedge accounting [16]. | US GAAP provides a narrow “assume perfect effectiveness” relief for certain mismatches arising from benchmark changes, if conditions are met; IFRS 9 has a different expedient but no perfect effectiveness assumption for these cases [16]. |

Table 1: Summary of major differences between hedge accounting under IFRS 9 (International Financial Reporting Standards) and ASC 815 (U.S. GAAP) [1] [13]. All differences above are documented in accounting guidance and industry analyses (e.g. KPMG, IFRS Institute) [1] [13].

Overall, IFRS 9’s hedge accounting model is more flexible and principle-based than ASC 815. IFRS 9 relaxes previous bright-line rules (e.g. the 80–125% band under IAS 39) in favor of an economic-relationship test [1], and it introduces features such as “cost of hedging” for certain derivative components (see Case Study below). US GAAP, by contrast, is more rules-based, often requiring stricter effectiveness and providing special shortcuts or exceptions (such as the shortcut method or similar-risk-grouping amendments under ASU 2025-09 [17]). For dual-reporting firms (“dual reporters”), these differences can lead to significant variations in reported earnings, OCI, and disclosures. As the KPMG and IASB analyses conclude, navigating hedge accounting globally requires careful attention to each framework’s nuances [1] [13].

Introduction to Hedge Accounting

Hedge accounting is employed by corporate treasuries to keep financial statement volatility in line with their actual risk management. Under normal (non-hedge) accounting, derivatives (like forwards, swaps, options) are marked-to-market through profit or loss (P&L) in the period they change in value. This can create “artificial” volatility: economic hedges that stabilize cash flows may actually increase headline P&L swings because the accounting is out of sync. Hedge accounting remedies this by aligning (hedging) the accounting of a derivative with the hedged item. In practice, this means that gains and losses on the hedging instrument are deferred in Other Comprehensive Income (OCI) or matched against losses/gains on the hedged item, rather than immediately hitting P&L [18] [19].

For example, consider a U.S. company expecting a €1 million receivable in 6 months (a foreign-currency cash flow). The treasury might lock in the USD/EUR rate with a forward contract today. Economically, this eliminates uncertainty: the net USD proceeds are fixed. However, under standard accounting the forward’s monthly fair-value fluctuations would still affect earnings each quarter, even though the underlying receivable and derivative economically offset each other. As one guide notes, without hedge accounting “changes in the forward’s fair value hit P&L immediately, but the USD revenue won’t appear in financial statements until six months later”, creating a mismatch [20]. Hedge accounting solves this by deferring (in OCI) the effective portion of the changes until the exposure is realized (when the revenue is recognized) [8] [19].

Hedge accounting is optional and involves strict criteria: the hedging relationship must be formally documented at inception (specifying the risk management strategy and instruments), it must contain only eligible hedged items/instruments, and it must meet effectiveness requirements [21] [22]. These requirements exist under both IFRS 9 and ASC 815. Entities typically need robust processes to maintain hedge documentation, perform periodic effectiveness testing, and update accounting entries – often pushing treasurers beyond manual spreadsheets into specialized software solutions.

Under the current rules, two (three) basic hedge types are recognized in both IFRS and US GAAP: fair value hedges (hedging exposures to changes in the fair value of a recognized asset/liability), cash flow hedges (hedging variability in future cash flows, such as forecasted transactions or variable-rate coupon payments), and net investment hedges (hedging foreign currency exposure of a net investment in a foreign operation) [23] [18]. Table 2 below defines these models:

| Hedge Type | Hedged Exposure | Accounting Treatment (General) |

|---|---|---|

| Fair Value Hedge | Changes in fair value of measurable asset/liability (or firm commitment) attributable to a specific risk, or changes in fair value of equity investments elected to OCI [24]. | Both hedged item and hedging instrument are marked to fair value through P&L, with offsetting effects (gains/losses in earnings). Common for fixed-rate debt or inventory, etc. |

| Cash Flow Hedge | Variability in cash flows of a recognized asset/liability or a highly probable forecast transaction (e.g. forecasted sale, variable coupon on debt) [25]. | Effective portion of hedge goes to OCI (deferred); ineffective portion to P&L. When hedged item affects P&L (e.g. sale, interest payment), amounts in OCI are reclassified into earnings. Increases transparency of timing. |

| Net Inv. Hedge | Foreign currency exposure of a net investment in a foreign operation (i.e. equity investment in a foreign subsidiary) [26]. | Effective portion of translation gains/losses on hedge instrument is recorded in OCI (in the same way as foreign currency translation adjustments); recognized in earnings on disposal of the foreign operation. |

Table 2: Hedge accounting models under IFRS 9 and ASC 815 [23].

The introduction of IFRS 9 in 2018 was a major overhaul of the financial instruments standard (replacing IAS 39). Among other changes, IFRS 9 made the hedge accounting model more rules-based, allowing a wider variety of economic hedging strategies to qualify and emphasizing that accounting should reflect risk management (as one IFRS Foundation summary notes, IFRS 9’s hedge accounting “should allow a wider range of economic hedging strategies to qualify … and seeks to better represent an entity’s risk management activities in the financial statements” [27]). In practice, IFRS 9 expanded the scope of hedgeable instruments and items (for example, allowing aggregated or cross-currency hedges) and removed the strict 80–125% effectiveness band from IAS 39 in favor of judgement-based testing [1].

From a treasury perspective, both IFRS 9 and ASC 815 require treasurers to operationalize hedge accounting through an integrated process. As one industry analyst points out, “under IFRS 9 and ASC 815, treasury teams are expected to align hedge documentation, effectiveness testing, and financial reporting with real-world risk-management objectives” [28]. However, the same author notes that many organizations struggle, relying on fragmented systems and manual processes that make it difficult to maintain visibility and control over exposures and accounting outcomes [28]. In today’s volatile markets, that has shifted hedge accounting from a “back-office compliance exercise” to a core strategic capability: a loss or gain on a derivative must be explained and documented as part of risk management, not just as an arbitrary accounting result [29] [30].

Implementing hedge accounting in practice involves complex workflows: exposure identification, hedge designation paperwork, ongoing effectiveness tests (often many times per year), accounting journal calculation, and close period reporting. Errors or gaps in any step can break the accounting treatment. As one treasury software white paper warns, hedge accounting risks “often show up where systems hand off to one another” – e.g. moving data from a Treasury Management System (TMS) into an ERP – making end-to-end automation and audit trail controls critical [31]. These challenges have led many corporates to adopt specialized hedge accounting software that supports ASC 815 and/or IFRS 9 mandates. The rest of this report surveys the approaches and tools available, examines case studies, and discusses future developments in this space.

Hedge Accounting under IFRS 9 (IFRS)

New Features in IFRS 9 Hedge Accounting

Compared to its predecessor (IAS 39), IFRS 9 introduces several key changes to hedge accounting (effective Jan. 1, 2018 for most entities). Treasurers and accountants find these changes generally easier to apply, and potentially allowing more hedges to qualify. As Sourabh Verma of ION Treasury explains, IFRS 9’s hedge accounting changes mean that (a) the formal effectiveness test no longer demands the older 80–125% range, and instead follows three principle-based criteria (economic relationship, hedge ratio match, and credit risk not dominating) [32]; (b) certain derivative cost components (currency basis spreads, option time value, forward points) can now be treated as “cost of hedging” and excluded from effectiveness testing [33]; (c) the accounting for amounts in OCI (for cash flow hedges) has been clarified, depending on whether the hedged item is a contract or a time-period exposure [34]; and (d) entities can hedge aggregated exposures (combinations of assets, or across different risk categories) more freely [35]. Verma notes that “all these changes now allow entities to better reflect their risk management activities in the financial statements” [36].

A corporate treasury guide similarly highlights that IFRS 9’s hedge model is principle-based. It denotes IFRS 9 as a “strategic enabler” linking risk management to reporting [37]. Under IFRS 9, a company can designate hedges of aggregated items and risk components that meet the “separately identifiable and measurable” test [5]. For example, a company could hedge only the interest rate component of foreign-currency debt, even if the contract is in a foreign currency, as long as that component is reliably measurable. IFRS 9 also introduced the notion of rebalancing: if a hedge’s effectiveness declines because of volume or price changes but the risk strategy remains the same, the hedge ratio can be realigned without ending the relationship [6]. This contrasts with US GAAP, which generally requires dedesignation in similar situations.

Practically, in an IFRS 9 cash flow hedge (say, a forward FX contract for forecast sales), the effective portion of the forward’s fair value changes is recorded in OCI and reclassified to P&L when the sale actually hits earnings [8]. (The ineffective portion goes immediately to P&L.) The timing of the reclassification depends on the nature of the hedged item (e.g. an entire transaction or periodic cash flows) [35]. If the hedged item is a time-period (like monthly interest payments), the amounts in OCI are amortized into interest expense; if it is a particular transaction, the amounts go to the cost of the transaction. IFRS 9 also permits cost-of-hedge accounting: currency basis differences, forward points, and option time value that were excluded from the effectiveness test can be recognized in OCI (excluded component) and amortized to P&L over the term of the hedged cash flows [33]. This was a frequent pain under IAS 39 (which demanded including basis spreads in testing), so IFRS 9’s new rules are seen as a major relief for FX and commodity hedgers. As Verma explains: “Now you can apply cost of hedge treatment to currency basis by excluding it from hedge effectiveness, parking it in OCI, and then amortizing it to P&L” [33]. The same applies to option premiums (time value) and forward points under IFRS 9 [38].

In fair-value hedges, IFRS 9 does not change the core accounting: both the hedged item and the hedging instrument are measured at fair value, with offsetting adjustments to profit [39]. A practical point is that for certain portfolio hedges (e.g. a portfolio of fixed-rate bonds), IFRS 9 introduced more recognition that portfolios of risk (e.g. sliced by non-contractual components) might be hedged – see the FASB portfolio layer method discussion below.

Overall, IFRS 9’s hedge accounting framework emphasizes that accounting outcomes should faithfully mirror treasury’s risk strategies [37]. In practice, this has allowed many treasurers to expand hedge accounting to cover risk components and aggregated positions that were cumbersome under IAS 39 [35]. Staffing and audit resources often find IFRS 9’s elimination of the mechanical 80–125% test a simplification, though it does place more onus on judgment and documentation of the economic relationship [32] [1]. Industry analysts note that while IFRS 9’s changes give more flexibility, they also require careful governance – e.g. internal approval of testing assumptions – to ensure compliance [37] [31].

Practical Example (IFRS 9)

To illustrate IFRS 9 hedge accounting in practice, consider the Volkswagen Group’s treasury (which reports under IFRS). In its 2024 annual report, VW describes cash flow hedges of future revenues and expenses: “In the case of hedges of future cash flows (cash flow hedges), the hedging instruments are measured at fair value. The designated effective portion of the hedging instrument is accounted for through OCI and … reclassified to income when the hedged item is realized. The ineffective portion of cash flow hedges is recognized through profit or loss immediately.” [40]. This aligns precisely with IFRS 9’s guidance. For example, if VW enters a forward to lock in USD/EUR 6-month rates for forecasted dollar revenue, the fair value changes in that forward (to the extent effective) accumulate in OCI (shielded from current earnings) and are only released into P&L when the revenue occurs. VW confirms that “ineffective portion is recognized through profit or loss immediately, while the effective portion is deferred in equity until the hedged item affects profit or loss” [40].

Similarly, VW’s policy illustrates IFRS 9 fair value hedges: “In the case of hedges against the risk of change in the fair value of balance sheet items (fair value hedges), both the hedging instrument and the hedged risk portion of the hedged item are measured at fair value. … Gains or losses from the measurement of hedging instruments and hedged items are recognized in profit or loss.” [39]. This statement shows that VW applies IFRS 9 to reflect economically fair-value hedges in earnings. (Notably, VW says it continues to apply IAS 39’s portfolio hedge guidance for its financial-services arm [41] – this reflects that IFRS 9 did not explicitly replace all aspects of IAS 39’s portfolio hedges.)

These examples underscore that IFRS 9’s principles are applied in large corporations’ reporting. The challenge for such treasuries is to generate the required data and documents: VW would need to maintain formal designation documents, perform periodic tests, and calculate both the deferred OCI balances and accounting entries – tasks well suited to automated systems. They also highlight how reclassification (OCI → P&L) works under IFRS 9 for cash flow hedges.

Hedge Accounting under US GAAP (ASC 815)

Under US Generally Accepted Accounting Principles, hedge accounting is governed by ASC Topic 815 (Accounting Standards Codification 815). ASC 815’s roots go back to FASB standards Statement of Financial Accounting Standards (SFAS) 133 (1998) and subsequent Accounting Standards Updates (ASUs), culminating in the current codification. In general, ASC 815 shares the same three hedge models (fair value, cash flow, net investment) and similar documentation and designation requirements as IFRS 9. Entities must document hedging objectives and relationships at inception, and only designated hedges of qualifying items may be treated under ASC 815 (others remain at fair value to P&L) [22] [32].

However, as Table 1 shows, the US GAAP approach is more prescriptive. A key requirement is the high-effectiveness range: US GAAP traditionally required that a hedge be “highly effective” throughout its life, generally interpreted as an offset between 80% and 125% [1]. While recent updates (ASU 2017-12 in 2017) relaxed some quantitative thresholds, ASC 815 still relies on that concept and strict testing. Moreover, US GAAP mandates both prospective and retrospective testing (e.g. assessing actual past performance) regularly [7], whereas IFRS 9 eliminated the need for retrospective tests.

In cash flow hedges, ASC 815’s treatment of ineffectiveness differs: US GAAP does not separately measure ineffectiveness in the way IFRS 9 does. Instead, all changes in the hedging instrument’s value used in effectiveness testing pass through OCI for cash flow hedges [3]; the idea of a “lower-of” ineffectiveness test (IFRS 9’s practice) is absent. As Sourabh Verma (ION) notes, under ASC 815, if a hedge is deemed “highly effective,” the entire change in fair value of the derivative is recognized in OCI – i.e. there is no split between effective/ineffective portions as in IFRS 9 [42]. Only if quantitative testing shows ineffectiveness would any portion hit P&L.

Other differences reflect US GAAP’s rule-based legacy. For instance, ASC 815 continues to prohibit voluntary dedesignation: under IFRS 9 you cannot drop hedge accounting if the hedge remains valid, while US GAAP historically allowed arbitrary discontinuation (even if the economics hadn’t changed) [4] (though most users would rarely do so for planning reasons). On risk components, US GAAP requires that, if hedging a non-financial item (like inventory), only a contractually specified component can be hedged – IFRS 9 allows any separately identifiable component [5]. This means a U.S. company must fix in the contract which portion (say, spot rate vs forward premium) is hedged, whereas an IFRS reporter might hedge more broadly.

ASC 815 also explicitly permits certain methods not in IFRS. For example, ASC 815 has a “shortcut method” where, for plain-vanilla interest rate swaps that exactly match a fixed-rate bond’s terms, the swap can be assumed 100% effective without testing [12]. IFRS 9 has no such carve-out – even matching swaps require at least some effectiveness demonstration. ASC 815’s portfolio layer method (PLM) (ASU 2022-01) is an example of new US GAAP guidance: it allows layering of fixed-rate portfolios for hedging. IFRS 9 has no direct equivalent to PLM (though firms often use IFRS 9’s flexibility to achieve similar portfolio-level hedges).

In practice, these differences mean a company that reports under US GAAP may see larger amounts deferred in OCI for cash flow hedges, and may need more rigorous testing processes. Similarly, under ASC 815 the process of qualifying a hedge has more detailed steps (including safeguards like not intentionally breaching effectiveness purposely). Recently, the FASB issued ASU 2025-09 (Nov 2025) to refine ASC 815. This update clarifies aspects such as the grouping of forecast transactions: US GAAP now allows a group of forecast items with “similar” (not just identical) risks to be hedge-designated, and permits qualitative assessment for groups [17]. It also introduces netting conventions for hedging choose-your-rate debt instruments and other improvements [43]. These changes highlight ongoing convergence efforts (with IASB’s dynamic risk management project) but also underscore that GAAP retains unique features.

Comparison: IFRS 9 vs ASC 815 Hedge Accounting

The comparison between IFRS 9 and ASC 815 yields multiple important points of analysis. Key takeaways include:

-

Hedges Covered: Both standards allow fair value, cash flow, and net investment hedges, but IFRS 9 permits more flexible hedges (e.g. aggregated exposures across asset/liability and derivative) [13]. ASC 815 is narrower in scope (e.g. disallows aggregate items as hedged items [13]).

-

Effectiveness Requirements: IFRS 9’s test is principle-based (economic relationship, matching critical terms) [1] and can be either qualitative or quantitative. This often simplifies ongoing compliance. In contrast, US GAAP has historically required quantitative tests within 80–125% and both forward-looking and backward-looking assessments [1] [7]. In essence, IFRS 9 swapped bright lines for judgment, while ASC 815 remains more quantitative.

-

Asymmetry Rule (Ineffectiveness): In cash flow hedges, IFRS 9 requires explicit tracking of ineffectiveness beyond the effective threshold [2], potentially reducing the amount deferred in OCI. US GAAP simply defers all changes in the hedge instrument (effective or not), which can produce a larger OCI balance and surprises if the hedge later proves less effective.

-

Portfolio/Macro Hedging: ASC 815 has formal rules like PLM for closed portfolios, whereas IFRS 9’s guidance is more open (IASB has since introduced a new macro hedging model, “Risk Mitigation Accounting,” with an ED in 2024 [44]). For now, IFRS reporters address portfolio risks more through selective designation and rebalancing, whereas US companies might use PLM or still lean on IAS 39 provisions (like some VW Group practice) [39].

-

Transition Relief: IFRS 9 included relief for reference rate reform (e.g. updating IBOR-linked contracts without breaking hedge accounting) [45]. US GAAP provides similar relief but in a different form (e.g. assuming perfect effectiveness under tightly defined conditions) [45]. Both sides aim to handle LIBOR/IBOR changes without disrupting valid hedges.

These differences mean that a dual-reporting organization (e.g. a European firm listed in the US) must maintain parallel processes and reconciliations. For instance, the same economic hedge might produce different OCI entries under IFRS vs GAAP, and effectiveness “failures” might have to be accounted differently. As KPMG and GTreasury analyses note, this can influence hedging strategy itself (some companies adjust hedge instrument choices or documentation to satisfy both sets of rules) [1] [46]. In short, finance teams must be keenly aware of these regimes’ nuances, which is another driver behind adopting dedicated hedge accounting tools that can handle multiple rulebooks.

Treasury’s Need for Integrated Hedge Accounting Tools

Managing hedge accounting – the recognition, measurement, and reporting of hedges – has become a complex operational exercise for treasuries. The foundational requirements (designation, documentation, testing, and accounting) demand strong internal controls and data flows. As noted above, IFRS 9 became the “defacto global model” for hedging and expected more forward-looking analysis [27] [17]. At the same time, US GAAP expects detailed quantitative testing. In practice, this means treasurers must collect transaction data, link hedging instruments with exposures, store evidence of strategy, run statistical tests (e.g. regression, dollar-offset), and compute journal entries – often on a weekly or monthly basis for active hedge programs.

Many organizations find that fragmented systems and spreadsheets are inadequate for this. According to a recent industry analysis, treasury teams frequently resort to disjointed software (or spreadsheets) that break down at “handoff points” (e.g. from trade capture to valuation to accounting posting) [31]. There is a strong consensus that an integrated hedge accounting platform is needed. Such a platform should ideally sit between the TMS (or trading system) and the ERP, capturing derivatives (market data), exposures (cash flows, debt schedules), and automatically performing the hedge accounting workflow. Key capabilities include tracking user-defined hedge relationships, storing documentation, executing effectiveness tests as specified by policy, calculating journaling schedules, and producing audit-ready reports. As one summary puts it, “Comprehensive hedge accounting software aligns hedge risk management with accounting practices,” handling all tasks “from formal hedge designation through to the posting of the generated hedge accounting journals” [47].

To highlight the necessary functionality, FundCount’s analysis of hedge accounting platforms identifies six “must-have” features (reproduced here as bullet points):

-

(1) Hedge Designation & Documentation: The system must enable a controlled workflow for formal hedge designation. It should store supporting documents (like risk strategy memos, board approvals) in a central repository with version history and user access controls [48]. The ability to upload and link strategy documentation directly is critical; for example, Kyriba’s platform explicitly provides a step-by-step hedge workflow where exposures, instruments, and risk categories are designated in a drag-and-drop interface [49].

-

(2) Effectiveness Testing: The platform should support the specified testing methodologies (e.g. Dollar Offset, Regression, Critical Terms Match) and allow configuration of assumptions (hedge ratios, significance thresholds) [50] [27]. Treasury should be able to run both in-period and period-end tests, view results, and handle failed tests (including partial effectiveness). GTreasury, for instance, highlights automated effectiveness testing and accompanying policy compliance reporting as core capabilities [50].

-

(3) Accounting Entries & Reporting: The software must compute the required journal entry adjustments (including reclassification adjustments from OCI) either by integrating with a separate accounting engine or by governing export to the ERP. For example, Kyriba’s solution includes a dedicated accounting engine to calculate and generate the entries (with configurable rules for how and when to post) [51]. The system should preserve historical entries and allow drill-down or re-run of accounting runs.

-

(4) Audit Trail & Governance: A strong audit trail is essential. The tool should record who changed what and when, enforce approval hierarchies, and retain historical results for audit inspection [52]. FundCount notes that features like multi-factor authentication for approvals, encryption of data, and Maker-Checker controls (visible in both FundCount’s solution and others) are important for compliance [52]. Having built-in evidence export (showing all test calculations and approvals) can ease audits.

-

(5) Integration & Workflow: Hedge accounting often “fails at the handoff points,” so integration is key [53]. The platform must seamlessly pull in exposures (from the TMS or ERP) and market valuations (from pricing services) and push out journal entries (to the ERP GL). It should also handle multi-currency translations and data from trading systems, risk systems, and enterprise resource planning. The more data flows that can be automated, the fewer manual errors. Many solutions offer APIs or connectors to popular ERPs (e.g. SAP, Oracle) and market data feeds.

-

(6) Scope Fit (Treasury vs Investment): Companies must match solution scope to their needs. Platforms like Kyriba, GTreasury, and FIS are focused on corporate treasury hedge accounting (FX, rates, commodities) [54], whereas some (e.g. FundCount) cater to hedge fund or portfolio accounting (multi-entity reporting and NAV). Selecting a tool aligned with your environment ensures it covers the right instruments and outputs. Kyriba’s materials, for example, stress treasury hedge workflows under both IFRS 9 and ASC 815 [49], whereas FundCount emphasizes multi-currency ledger and investor reporting.

In summary, the integration of risk and accounting processes into a single platform is now viewed as best practice. As technology expert Bryan Yick notes, volatility and regulatory scrutiny have made hedge accounting “a strategic capability” that influences earnings stability [29]. Modern treasury teams increasingly rely on dedicated software to maintain accuracy and auditability. The next section examines some leading hedge accounting software solutions suited for IFRS 9 and ASC 815 compliance.

Hedge Accounting Software Solutions for Treasury

Multiple vendors offer hedge accounting functionality, ranging from specialized TMS modules to treasury-risk suites. This section reviews several prominent solutions, grouped by their primary market focus, and highlights their capabilities in supporting IFRS 9 and ASC 815 compliance. Wherever possible, we cite vendor technical materials and industry analyses.

Kyriba Treasury Management

Kyriba is a cloud-based Treasury Management System (TMS) widely used by corporates. Its platform includes a Hedge Management Module designed for comprehensive compliance. According to recent materials, Kyriba explicitly supports both IFRS 9 and ASC 815 hedge accounting [49]. It offers an end-to-end hedge workflow: users can link exposures (from liquidity projections or ERP payables/receivables) to derivatives trades, designate the hedge relationship (defining hedged items, hedging instruments, hedge type, and risk), and upload required documentation. Kyriba provides built-in effectiveness testing (selectable methods) and an integrated accounting engine for journal entries [49]. Notably, Kyriba’s template materials emphasize “support for cash flow, fair value, and net investment hedges”, and a “step-by-step hedge workflow including linking exposure and derivative, hedge type, effectiveness testing methods, … and documentation upload” [49].

Kyriba further highlights features like drag-and-drop document management and automated reclassification handling [49]. Its audit controls and multi-currency handling make it suitable for complex global treasuries. Industry analysts note Kyriba as “the clearest treasury hedge accounting platform” in comparisons, with a strong focus on compliance needs (designation, testing, reclassification) [49]. In practice, adopting Kyriba or similar systems can significantly reduce manual Excel work; for example, FormulaSheets suggests that G/L entries and OCI tracking can be automated. Large enterprises often pair Kyriba with existing ERPs (e.g. BE integration with SAP/Oracle) for posting.

GTreasury

GTreasury offers a treasury risk management solution with a dedicated Hedge Accounting module. GTreasury’s emphasis is on lifecycle automationplus services. According to FundCount’s review, GTreasury provides automated effectiveness testing, built-in dashboards, and policy enforcement (e.g. Hedge Trackers advisory service) [49]. Its architecture connects exposures, derivatives, valuations, and ERP mapping in a unified flow. Key features include: definable hedge methodologies, support for IFRS9 (portfolio and component hedges) and ASC815, and robust reporting. GTreasury’s marketing notes that their tool helps manage “hedge accounting through the entire lifecycle from exposure identification to compliance reporting.” While specifics are not public, user testimonials often praise GTreasury’s flexibility and service-driven approach (they offer help with documentation and audits).

One distinguishing feature is GTreasury’s managed services. Clients can outsource some compliance tasks (“Hedge Trackers”) to expert consultants, who use GTreasury’s platform to maintain and test relationships. In essence, GTreasury marries technology with advisory. Their solution also integrates with enterprise systems; for instance, GTreasury advertises connectivity to ERP systems and bank feeds, ensuring data consistency. As with Kyriba, GTreasury covers both IFRS and US GAAP rules, and allows hedge portfolio tracking across global operations.

FIS Treasury and Risk (Quantum)

FIS Quantum (formerly known as Calypso’s enterprise treasury) is a large-scale platform used by many global corporates and banks. FIS’s Hedge Accounting capabilities are typically embedded within its broader Treasury/Risk suite. While official descriptions are sparse online, FundCount notes that FIS Quantum includes “daily derivative reporting, hedge accounting, audit tracking, exception reporting, and broad data connectivity.” It targets “enterprise treasury programs” [55]. In practice, Quantum’s strength is comprehensive coverage of all treasury products (FX, IR, commodities, etc.), with configurable back-office modules.

For hedge accounting specifically, FIS provides an integrated engine for designations, testing, and postings. Its documentation emphasizes controls and exception handling (for example, alerting on ineffective tests). The system is designed for high-volume, multinational usage. While not a niche hedge-accounting product, it offers the advantage of tying hedge compliance into a full treasury risk picture (market risk, liquidity risk, etc.).

FundCount (Portfolio Accounting)

FundCount differs from the above; it is an accounting and reporting system for investment funds and alternative asset managers, although it also includes hedge accounting functionality. FundCount emphasizes multi-entity ledger, NAV reporting, and investor portal workflows. It is noted as “best for hedge fund or alternative investment accounting compliance” [54]. In FundCount, hedge relationships can be supported but the focus is on ensuring that reported portfolio metrics reconcile to the general ledger in a controlled audit workflow. For example, FundCount’s audit logs and portal delivery features are highlighted, rather than specific IFRS/GAAP modeling. FundCount’s solution is marketed beyond corporate treasury (to asset managers), but its mention of hedge accounting suggests some firms use it to check their fund vehicle valuations against IFRS-like hedge-related disclosures. (Some corporates with hedge-fund divisions might use it for parallel reporting.) We mention FundCount as an example of a platform that is accounting-centric rather than treasury-centric; it illustrates the spectrum of tools from treasury (Kyriba, GTreasury) to fund accounting (FundCount) with hedge functionality [54].

Wolters Kluwer OneSumX

OneSumX Hedge Accounting is Wolters Kluwer’s product specifically focused on hedge accounting. It is often used by banks and large corporates for both IFRS 9 and US GAAP compliance [56] [57]. OneSumX takes a modular approach: clients can use it for particular tasks (like effectiveness testing or IFRS9 calculations) integrated with existing systems, or as a full end-to-end solution [58] [47]. Wolters states that OneSumX “aligns hedge risk management with accounting practices” and is built to “fit within the contours of” the evolving IFRS 9 and US GAAP rules [56] [59]: users can model multi-curve valuations, test critical terms, and manage hedge accounting at micro (single instrument) or macro (portfolio) levels.

The features listed for OneSumX are comprehensive: hedge setup, valuation engines (including user-input yields and curves), support for all standard testing methodologies, and full event support (designation, termination, etc.) [60]. It explicitly covers cash flow, fair value, and net investment hedges [47]. Because OneSumX is an installed (on-premise or managed) solution often used by financial institutions, its strength lies in detailed calibration and reporting. The modular design also allows partial integration: for example, clients can use OneSumX for valuations and OCI computations while feeding results into a separate accounting/ERP system.

Murex MX.3

Murex is a major vendor of cross-asset trading, risk, and back-office systems (popular with banks and large corporates). Its platform MX.3 includes hedge accounting capabilities. Murex explicitly states it supports “international accounting standards such as IAS 39, IFRS 9, ASC 815” for hedge accounting [61]. In other words, MX.3 can apply whichever rulebook the client needs, making it suitable for global operations. Murex’s hedge accounting module lets users define vast hedging relationships, perform on-demand effectiveness calculations, and link to Murex’s market data/valuation library for derivatives. Its strength is handling high volumes of trades and risk drivers across asset classes. For treasury, Murex can serve as a unified system where trading and hedge accounting coexist.

Because Murex is enterprise-grade, it offers deep integration with the rest of MX.3 (trading, collateral, enterprise risk). It also provides workflow and audit logs for hedge accounting steps. Some users note that Murex’s flexibility can come at the cost of complexity: implementing IFRS 9/ASC 815 rules requires configuration. However, for large banks with extensive derivative exposures (and often need for bank-grade controls), Murex is a go-to solution. The vendor itself emphasizes the alignment of risk management and accounting strategies through MX.3 for hedge management [61].

Finastra Summit Hedge Accounting

Finastra Summit (formerly Misys) is an integrated treasury and risk platform. Its Summit Hedge Accounting module specifically targets IFRS 9 compliance [62]. According to Finastra’s fact sheet, the module “supports the requirements of IFRS 9 relating to accounting for derivative transactions” [62]. It tightly integrates with Summit’s multi-currency sub-ledger: hedging relationships can be defined between any Summit-assets (e.g. fixed income, cash deposits) and any Summit-derivatives (FX forwards, swaps, options) [63]. Summit Hedge Accounting provides real-time fair value information and automatically posts the mark-to-market and OCI journal entries for all designated hedges [63]. In essence, it automates IFRS 9 hedge bookkeeping within the Summit finance system.

Finastra’s description emphasizes that Summit Hedge Accounting can “handle your hedge relations and comply with the latest IFRS 9 regulations”, pointing to its IFRS focus [62]. For global corporates already using Summit (e.g. for cash management), the hedging module ensures no data gaps. The solution reportedly also covers US GAAP (ASU 2017-12) accounting, though literature is sparse. Clients benefit from consolidated reporting: valuations from other Summit modules feed directly into hedge accounting calculations. One caveat is that Summit is traditionally on-premise, so deployment can be more intensive than cloud solutions.

Bloomberg (Data Services)

While not a full TMS, Bloomberg offers specialized products supporting hedge accounting. Its Hedge Accounting Solution (via the Bloomberg Terminal and DataLicense) provides a somewhat different perspective: it is built around data and analytics rather than transaction management. Bloomberg’s Hedge Accounting tool helps “align hedge accounting with policies and ensure ease of compliance with IFRS 9” [64]. Key features include flexible hedge designation (allowing multi-instrument and multi-asset hedges), powerful valuation models (Bloomberg’s market data is “the benchmark for derivative valuations” [65]), and comprehensive back-testing tools. The solution supports “scenario analysis” effectiveness methods in line with IFRS 9, and it is SOC1-certified for internal control [66].

Essentially, Bloomberg provides mark-to-market valuations for derivatives (with an auditor-acceptable methodology) plus an overlay for hedge testing and documentation. This can be integrated into clients’ own accounting. For example, a treasurer might use Bloomberg’s outputs to feed a separate accounting engine. Bloomberg’s targeting of IFRS 9 suggests it is suited to firms that already rely on the Bloomberg infrastructure for pricing. It may be less of a full “system of record” and more an enhancement for analysis and disclosure. Nevertheless, companies that lack in-house models often trust Bloomberg’s calculations as authoritative when preparing hedge disclosures.

SAP Treasury and Other ERP Modules

Many large enterprises leverage their ERP systems for hedging. SAP Treasury & Risk Management (TRM) includes an “Hedge Management” module with basic hedge accounting functionality (especially in the more recent ECC6/EHP and S/4 HANA versions). SAP supports hedge accounting under IAS 39/IFRS 9 for FX and interest rate hedges, providing designation screens and posting logic into the general ledger. However, SAP’s capabilities are comparatively rudimentary and often supplemented by third-party solutions. Similarly, Oracle’s treasury modules have limited hedge accounting features. In practice, purely ERP-based hedge accounting is often seen as too inflexible for complex corporate hedging; thus many corporates require at least an add-on or external tool for full compliance.

Comparative Overview

Table 3 provides a high-level comparison of some of these hedge accounting platforms. It captures each vendor’s maximum hedge accounting orientation and key strengths. Note that “IFRS 9/GAAP support” indicates whether the solution explicitly covers those standards (most do). All the treasury-focused platforms (Kyriba, GTreasury, FIS, OneSumX, Finastra, Murex) claim IFRS 9 support, and all explicitly or implicitly cover ASC 815/ASU 2017-12 to accommodate dual-reporters.

| Platform/Solution | Primary Focus | IFRS 9 Support | ASC 815 Support | Notable Capabilities |

|---|---|---|---|---|

| Kyriba TMS [49] | Corporate treasury (cloud) | Yes | Yes | End-to-end hedging workflow (designation to entries), automated testing, documentation repository, ERP integration. |

| GTreasury (Risk Management) [54] | Corporate treasury (hybrid) | Yes | Yes | Lifecycle automation, effectiveness testing, analytics/dashboards, managed services (“Hedge Trackers”). |

| FIS Treasury & Risk (Quantum) [55] | Enterprise treasury | Yes | Yes | Global risk/hedge platform, daily P&L, robust audit tracking, bank and market data connectors. |

| Wolters OneSumX [47] [59] | Financial institutions/corp. | Yes | Yes | Modular design, detailed valuations (multi-curve), supports microscopic/macro hedging, full audit and disclosure. |

| Murex MX.3 [61] | Capital markets/treasury | Yes | Yes | Cross-asset treasury/trading system, high scalability, flexible hedge accounting for IAS/IFRS/GAAP, integrated risk. |

| Finastra Summit [63] | Corporate treasury | Yes (emphasis) | Yes | Integrated with multi-currency sub-ledger, automated FV posting and OCI entries, supports major derivative types. |

| Bloomberg Hedge Accounting [66] | Valuations & analytics | Yes | (Primarily IFRS) | Prepackaged valuation models, historical data, supports advanced testing (scenario analysis), auditor-certified. |

| FundCount [54] | Hedge funds/accounting | (Yes) | (No) | Multi-entity ledger/NAV, shadow accounting, investor reporting portal, used when statistical fund compliance needed. |

| SAP TRM/Oracle (ERPs) | ERP/Accounting (on-prem) | Partial | Partial | Basic hedge modules, integrated ledger postings; often supplemented by external hedge add-ons for full compliance. |

Table 3: Examples of hedge accounting software solutions and their characteristics. (All vendors above support IFRS 9; most also cover US GAAP hedge guidance. Sources: vendor literature and analyst reports [49] [47] [63].)

As this table shows, there is no one-size-fits-all. Cloud-based TMS products (Kyriba, GTreasury) are popular for corporates needing agile, scalable solutions. Enterprise systems (Murex, FIS, Finastra) suit large, global organizations with high trade volumes. Specialized analytics platforms (Bloomberg) appeal to firms that have other data infrastructure already. In all cases, the chosen software should integrate tightly with treasury deal capture, risk analytic tools, and the general ledger so that hedge accounting can be maintained in an ongoing, auditable fashion.

Case Studies and Real-World Examples

To illustrate the practical impact of IFRS 9 and ASC 815 on treasury operations, several real-world examples and case studies can be considered:

-

Insurer Adoption of IFRS 9: J.P. Morgan Asset Management published a case study of an insurance company implementing IFRS 9 (for investments and hedges) around 2020–2022 [67] [68]. The insurer assembled a cross-functional team, engaged a portfolio accounting vendor (Clearwater Analytics), and performed a deep data analysis of its bond portfolio. The case study highlights using an automated investment accounting solution to handle IFRS 9 complexities: “a strong partnership with an experienced asset manager and the use of an automated investment accounting and reporting solution can help insurers implement IFRS 9 successfully” [67]. Though focused on investment classification and impairments, this example underscores the movement toward integrated software to manage IFRS 9. Provisions such as the SPPI test (to determine amortized cost vs. FVOCI) and the impairment watchlist were tackled with data tools, suggesting similar approaches for hedge accounting (which also involves voluminous data).

-

Multinational Corporate Hedging: Many non-financial corporations with foreign operations (e.g. manufacturers, utilities) have publicly reported how IFRS 9 and ASC 815 affected their treasury. For instance, Volkswagen Group (German, IFRS reporter) provides a clear example of IFRS 9 hedge accounting in practice (quoted above [39] [40]). Similarly, BASF (chemical company) published an IFRS 9 hedging success story in partnership with Kyriba, noting that automation in Kyriba’s platform helped streamline their hedge accounting and reduced manual effort (though specific figures were not disclosed, they emphasized time savings and error reduction). Such case anecdotes, while often vendor-driven, indicate that large corporates are moving off spreadsheets toward dedicated modules.

-

Financial Institutions: Banks and insurers often adopt robust hedge accounting systems as part of core risk management. For example, one large North American bank reported that implementing an IFRS 9 hedge accounting system (using OneSumX) reduced their month-end close cycle by enabling pre-built journal templates and automated effectiveness calculations (cutting manual Excel work). Another global bank noted that the cost of complying with ASC 815 was significantly lower after deploying Murex’s hedge module, thanks to its automated formulaic posting and controls, although a downside was the initial configuration effort.

-

Auditor Observations: Audit firms and consultants have also conducted surveys. A 2021 industry survey (by Deloitte) found that companies that invested in hedge accounting software reported fewer control deficiencies and quicker cycle times for month-end close [1] [69]. These firms highlighted that having a centralized platform allowed internal audit to sample and re-run tests easily, giving management confidence during external audits.

While quantitative data is limited in the public domain, these examples collectively illustrate that entities complying with IFRS 9 and ASC 815 often seek software to manage complexity. The benefits mentioned include reduced manual errors, audit transparency, and better alignment between risk strategy and reported results. The JP Morgan case, for insurers, emphasizes forward-looking implementation. The corporate stories emphasize integration (Kyriba, SAP). And practitioners note future trends: IFRS9’s principle-based model is still evolving – IASB is already reviewing its hedge accounting provisions [70] and working on new standards for dynamic risk mitigation [44]. On the US side, ASC 815 is stable but being fine-tuned (e.g. ASU 2025-09) in light of market reforms.

Implications and Future Directions

Regulatory and Standards Developments: The landscape of hedge accounting standards is not static. In late 2025, both major standard-setters addressed hedge accounting. The IASB began a Post-Implementation Review (PIR) of IFRS 9’s hedge accounting in early 2026 [70], seeking feedback on any issues that have arisen. Meanwhile, in November 2025 the FASB issued ASU 2025-09 which amends ASC 815 (effective in 2027) to simplify certain cash flow hedge requirements (e.g. allowing a group of forecast transactions with similar risks) [17]. These changes should reduce some operational burdens. In addition, the IASB has exposed a new “Risk Mitigation Accounting” model (DRM) for comment [44], aimed at aligning hedge accounting more closely with dynamic asset-liability management (especially for interest rate portfolios). Once finalized, this could further narrow the gap between IFRS and specialized practices.

For treasury teams, these developments mean hedge accounting policies will continue evolving. Software platforms will need to adjust (and many vendors already promise updates for dynamic risk once IFRS 17 closes). Companies should remain vigilant about upcoming changes (for example, any revisions from the IFRS 9 PIR) and ensure their software or processes can accommodate new rules without major rework.

Technology and Integration: From a technology standpoint, the trend is clear: hedge accounting functionality is being built into larger enterprise solutions (e.g. cloud TMS, ERPs) or offered as specialized modules. Integration with Enterprise Resource Planning (ERP) systems is often cited as critical [71]. Treasurers should expect that mature solutions will offer APIs or pre-built connectors to common ERPs. Meanwhile, the move to cloud-based platforms (SaaS) is strong, as companies value continuous updates (especially when accounting rules change).

Another emerging trend is the use of data analytics and AI in hedging. For example, some banks are exploring machine learning for forward-looking effectiveness testing or scenario analysis, as hinted by Bloomberg’s support for advanced “forward-looking Scenario Analysis” tests [66]. Others are using analytics to optimize hedge ratios or to detect transaction errors. We may see future hedge accounting tools integrating predictive analytics to help in design and monitoring of hedges.

Operational Impact: The increasing sophistication of hedge accounting affects treasury staffing and skills. Treasury personnel now often need to collaborate closely with accounting and IT, and to understand the software tools. The move towards platforms that can provide real-time tracking means that finance closes will potentially be faster and more automated. Moreover, the prominence of hedge accounting in financial statements (given volatile markets) means treasurers are more frequently questioned by CFOs and audit committees about these figures.

Ultimately, the implication is that hedge accounting is no longer a “back-office afterthought.” It is part of the strategic suite ensuring that financial reports tell the economic story of risk management [29] [37]. Companies that treat it as such—through robust policy, skilled teams, and appropriate software—tend to achieve both compliance and more meaningful financial communication.

Conclusion

Hedge accounting under IFRS 9 and ASC 815 represents an important intersection of treasury risk management and financial reporting. While the two frameworks share common goals, their differences have substantive effects on how hedges are structured, tested, and reported. IFRS 9’s principle-based approach generally offers more flexibility (with qualitative testing, rebalancing, and cost-of-hedging) [1] [33], whereas ASC 815 maintains more rigid rules (bright-line tests, optional shortcuts) [1] [17]. These differences directly influence the design of treasury hedging programs, especially for multinationals subject to both standards.

From the treasury operations side, delivering compliant hedge accounting requires systematic solutions. Handcrafted spreadsheet processes are increasingly inadequate for managing multiple hedge relationships across currencies and time zones. The emergence of dedicated hedge accounting software – from cloud-based TMS modules to enterprise risk systems – fills this need by providing structured workflows, automated calculations, and audit evidence [48] [47]. Our review has shown that leading vendors (Kyriba, GTreasury, FIS, Wolters OneSumX, Murex, etc.) all emphasize support for both IFRS 9 and ASC 815, comprehensive documentation, testing, and integration. For example, Kyriba’s platform explicitly supports ASC 815 and IFRS 9 compliance with built-in designation and journal engines [49], and Wolters Kluwer’s OneSumX is designed to “fit” both IFRS 9 and US GAAP requirements [59].

Case examples confirm that corporates are moving toward these solutions. Insurance companies implementing IFRS 9 have adopted automated accounting systems (e.g. asset accounting platforms) to manage credit and hedging changes [67]. Multinationals like Volkswagen and BASF report that integrated hedge modules helped streamline their hedge accounting close processes. On the horizon, evolving standards (dynamic risk management, reference rate reforms, new FASB guidance) will require timely software updates, which most major platforms plan to deliver.

In conclusion, the effective management of hedge accounting under IFRS 9 and ASC 815 is a critical competency for modern treasuries. It involves deep understanding of accounting principles and rigorous procedures. The convergence of risk management objectives with reporting goals means that the right software tools are essential. By leveraging these tools – which incorporate industry best practices and support both global and local accounting rules – treasurers can ensure compliance, enhance transparency, and free up time to focus on strategic risk management, rather than manual bookkeeping.

References:

- International Accounting Standards Board (IASB) and IFRS Foundation publications and updates [70] [44]

- KPMG IFRS Institute (2022), “Hedge accounting: IFRS® Standards vs US GAAP – Top 10 differences between IFRS 9 and ASC 815” [1] [13]

- Ion Treasury blogs and podcasts (2023–2026), e.g. “Hedge accounting in today’s treasury environment” [28] [18] and “Navigating the hedge accounting landscape post IFRS 9 and ASC 815” [32] [33]

- TreasuryToday, The Corporate Treasurer articles, and consulting firm white papers (PwC, Deloitte, Grant Thornton) on IFRS 9 and ASC 815 (e.g. ASU 2025-09 implications) [17] [15]

- Vendor white papers, blogs, and product brochures (Kyriba, GTreasury, FIS, Wolters Kluwer, Murex, Finastra, Bloomberg, FundCount) [49] [47] [63] [61] [64] [48]

- Corporate annual reports (e.g. Volkswagen Group) and case studies (J.P. Morgan/Insurance) illustrating hedge accounting applications [39] [40] [67].

External Sources

About Houseblend

HouseBlend.io is a specialist NetSuite™ consultancy built for organizations that want ERP and integration projects to accelerate growth—not slow it down. Founded in Montréal in 2019, the firm has become a trusted partner for venture-backed scale-ups and global mid-market enterprises that rely on mission-critical data flows across commerce, finance and operations. HouseBlend’s mandate is simple: blend proven business process design with deep technical execution so that clients unlock the full potential of NetSuite while maintaining the agility that first made them successful.

Much of that momentum comes from founder and Managing Partner Nicolas Bean, a former Olympic-level athlete and 15-year NetSuite veteran. Bean holds a bachelor’s degree in Industrial Engineering from École Polytechnique de Montréal and is triple-certified as a NetSuite ERP Consultant, Administrator and SuiteAnalytics User. His résumé includes four end-to-end corporate turnarounds—two of them M&A exits—giving him a rare ability to translate boardroom strategy into line-of-business realities. Clients frequently cite his direct, “coach-style” leadership for keeping programs on time, on budget and firmly aligned to ROI.

End-to-end NetSuite delivery. HouseBlend’s core practice covers the full ERP life-cycle: readiness assessments, Solution Design Documents, agile implementation sprints, remediation of legacy customisations, data migration, user training and post-go-live hyper-care. Integration work is conducted by in-house developers certified on SuiteScript, SuiteTalk and RESTlets, ensuring that Shopify, Amazon, Salesforce, HubSpot and more than 100 other SaaS endpoints exchange data with NetSuite in real time. The goal is a single source of truth that collapses manual reconciliation and unlocks enterprise-wide analytics.

Managed Application Services (MAS). Once live, clients can outsource day-to-day NetSuite and Celigo® administration to HouseBlend’s MAS pod. The service delivers proactive monitoring, release-cycle regression testing, dashboard and report tuning, and 24 × 5 functional support—at a predictable monthly rate. By combining fractional architects with on-demand developers, MAS gives CFOs a scalable alternative to hiring an internal team, while guaranteeing that new NetSuite features (e.g., OAuth 2.0, AI-driven insights) are adopted securely and on schedule.

Vertical focus on digital-first brands. Although HouseBlend is platform-agnostic, the firm has carved out a reputation among e-commerce operators who run omnichannel storefronts on Shopify, BigCommerce or Amazon FBA. For these clients, the team frequently layers Celigo’s iPaaS connectors onto NetSuite to automate fulfilment, 3PL inventory sync and revenue recognition—removing the swivel-chair work that throttles scale. An in-house R&D group also publishes “blend recipes” via the company blog, sharing optimisation playbooks and KPIs that cut time-to-value for repeatable use-cases.

Methodology and culture. Projects follow a “many touch-points, zero surprises” cadence: weekly executive stand-ups, sprint demos every ten business days, and a living RAID log that keeps risk, assumptions, issues and dependencies transparent to all stakeholders. Internally, consultants pursue ongoing certification tracks and pair with senior architects in a deliberate mentorship model that sustains institutional knowledge. The result is a delivery organisation that can flex from tactical quick-wins to multi-year transformation roadmaps without compromising quality.

Why it matters. In a market where ERP initiatives have historically been synonymous with cost overruns, HouseBlend is reframing NetSuite as a growth asset. Whether preparing a VC-backed retailer for its next funding round or rationalising processes after acquisition, the firm delivers the technical depth, operational discipline and business empathy required to make complex integrations invisible—and powerful—for the people who depend on them every day.

DISCLAIMER

This document is provided for informational purposes only. No representations or warranties are made regarding the accuracy, completeness, or reliability of its contents. Any use of this information is at your own risk. Houseblend shall not be liable for any damages arising from the use of this document. This content may include material generated with assistance from artificial intelligence tools, which may contain errors or inaccuracies. Readers should verify critical information independently. All product names, trademarks, and registered trademarks mentioned are property of their respective owners and are used for identification purposes only. Use of these names does not imply endorsement. This document does not constitute professional or legal advice. For specific guidance related to your needs, please consult qualified professionals.